The economic damage caused by the restrictive official measures in the fight against the spread of the corona virus take on enormous dimension.

The global economy is therefore threatened by the most severe crisis by far in the post-war period. While China experienced the economic slump in the first three months of the year, the effects of the corona crisis were felt in the USA, Europe and the rest of the world, they only became apparent towards end of the first quarter and to their full extent at the beginning of the second quarter. As a result, the growth forecast for the global economy was again adjusted significantly downwards.

Tactical Asset Allocation

|

Liquidity |

Overweight |

|

Bonds |

Neutral |

|

Equities |

Underweight |

|

Alternative Investments |

Neutral |

The deep fall in the global economy is also reflected in the current economic data. In the latest purchasing manager survey the PMIs in virtually all countries to new historic lows. Unlike in “normal” recessions, in which the cyclical industrial sector suffers the sharpest slump, this time the service sector bears the brunt of the crisis. In view of closed shops, restaurants, limited services and a lack of travel, this is not surprising, but it does intensify the economic downturn. The picture on the labour markets is also darkening dramatically. For example, the number of first-time applications for unemployment benefits in the US shot up by more than 26 Mio. in just five weeks. Analysts expect that in the next few weeks more workers will slip into unemployment and that a total of 35 – 40 Mio. people will apply for these benefits by the end of May. That would be around a quarter of all employees. In Europe as well, unemployment figures will rise significantly, albeit with a time lag and to a lesser extent, thanks to the instrument of short time working.

However, the US economy will not reach its pre-crisis level before 2022. The crash is alleviated by the central bank, which has moved from the Lender of Last Resort to Buyer of Last Resort. Since the beginning of the crisis, it has expanded its balance sheet by over 2’000 trillion, thus helping to calm the financial markets. Meanwhile, the government is supporting households and businesses to mitigate possible second-round effects. In view of the enormous expenditure, the budget deficit will reach 18 percent of GDP in the current year alone.

In any case FED President Powell left a few strong hints that he is prepared to do more and is expecting to do more on yesterday’s FOMC Meeting. The FED put is in play. If there is any trouble, they are going to deliver more.

Looking at the EZ, the deep recession is also leading to a sharp increase in public debt due to the extensive stimulation measures. However, because the ECB is keeping interest rates very low through record high purchases of securities, debt servicing takes up a much smaller share of the government budget than during the financial crisis. From today’s perspective, a renewed debt crisis is not to be expected.

Fixed Income

In April, Fixed Income was mainly driven by credit markets. US 10yr rates traded within a narrow 20 bps range, compared to 60 bps one month ago. US 10yr rates found their level close to the lows as data show a dramatic deterioration in the US economy. Manufacturing, employment and consumer data dropped massively. Similar picture we see in the Eurozone.

In credit, the HY sector got most of the attraction with the move by the FED to buy low-rated bonds and even exchange traded funds of junk debt. This unprecedented scheme was the signal for a 250 bp rally in US HY. But half of the tightening was evaporated by a crashing oil price. Investment Grade corporates had their best month since 2008 on the back of the FED buying.

The primary market for riskier credits was reopened again, with many deals heavily oversubscribed. Even hardest hit sectors like cruise lines, hotels, cars etc. were able to print, although with high concessions. Companies are trying to set up cash buffers in order to be prepared for the economic downturn.

EM bonds were not able to follow the rest of the credit market. The missing FED-bazooka and a crashing oil price were responsible for a flat performance. Rating agencies have been active everywhere. Most of the downgrade focus got the Mexico/Pemex space with forced selling from institutional accounts.

Although overall HY levels look still attractive, we prefer to be selective and expect current risk-on sentiment to be tested by weak economic data.

Equities

Equity markets are holding surprisingly well in view of the severity of the economic crisis. The unprecedented aid packages of the governments are having a calming effect on investors. At the same time, the ultra-expansive monetary policy of the central banks is ensuring permanently low yields.

Equity Indicators*

|

Valuation |

Negative |

|

Momentum |

Neutral |

|

Seasonality |

Attractive |

|

Macro |

Negative |

The MSCI World gained more than 10 percent the last four weeks. All regions ended the month in positive territory. North America was one of the main winners. Within sectors, financial services and industrials, energy continued their relative weakness. Once again, health and technology led the field. Cyclical consumption recovered strongly, partly because of the slow normalization in the important sales market of China and the prospect of this in the rest of the world.

Source: Bloomberg, Clarus Capital

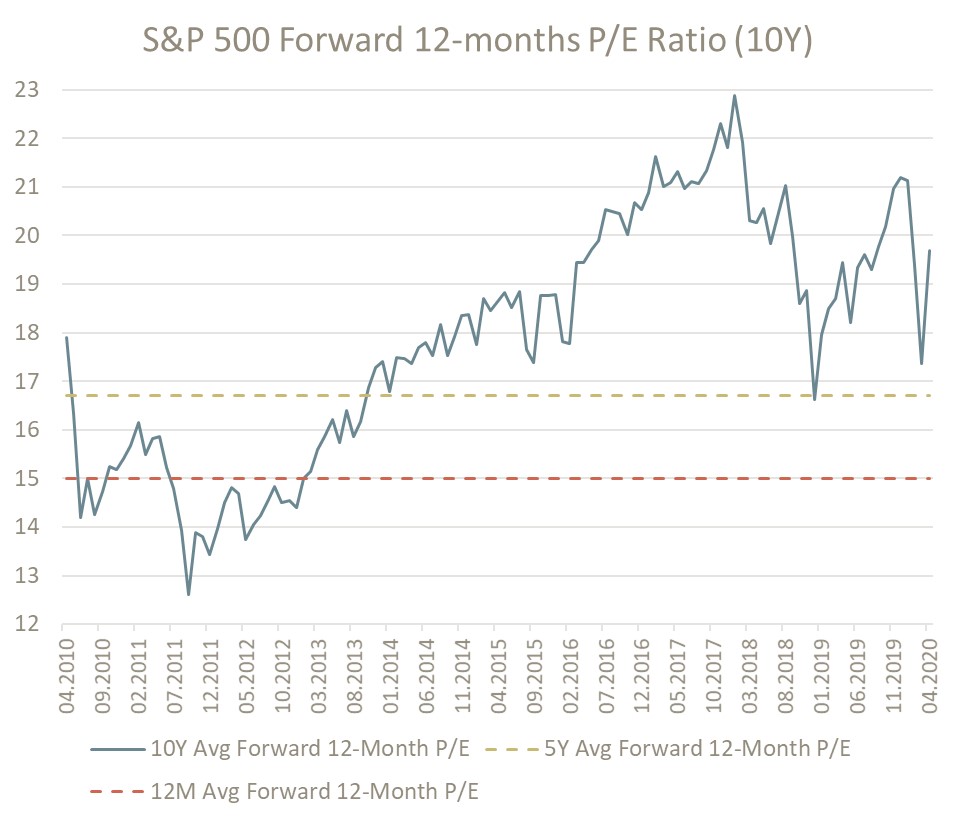

Whilst being in the Q1 earnings season, so far, the expectations have been disappointed. A number of companies are having difficulty providing an estimate for the future earnings due to uncertainty in the current environment. But looking at the 10Y P/E Ratio compared to its 12M and 5Y average we can clearly see S&P companies are now still trading at expensive valuation for the cycle, despite the historical crash, high volatility and wider spreads.

The S&P 500 is almost as expensive as before the markets started to collapse. Investors may be optimistic by paying 19x should we see a strong rebound in economic activity and validating a V-shaped pattern for economic growth. We highly doubt this scenario with negative fundamentals ahead of us and we might see markets to retest new lows.

Hence, we remain underweight in Equities and are biased to companies, sectors which are well positioned for the journey and destination. Two key points should investors have an eye on for the months to come: the extend to with the markets are factoring in the other side of the “U” – and more important is that the comfort the market has in the FED being there to backstop.

Alternatives

As for the oil market, which we covered just recently, we might have seen just a glimpse of what is to come for the weeks and months. Oil prices will most likely remain under pressure alongside the energy sector.

With major central banks moving interest rates to zero or below we can expect investors to move into gold as bond yields are reduced and the risk of inflation increases that would devalue other assets and currencies but subsequently adds to the value of gold. Having floated the markets with liquidity and uncertainties remain on coronavirus impact, we suggest adding gold when we see a pullback.

In the FX space the USD remains the main driver. Even though the greenback should depreciate with all these liquidity measures from the central banks, corporates and institutional buyers prefer to add their cash quota and, hence buying USD. Also, the greenback has a sense of risk-off element which we have perfectly seen as stocks fall. At the same time, just be mindful that it is still month-end trading and hence, positioning flows are also a factor to consider in this environment.

Note: This report is published by Clarus Capital Group AG

Roger Ganz

Head Asset Management, Clarus Capital Group AG

Dejan Ristic

Partner, Clarus Capital Group AG

Disclaimer

This document has been prepared by Clarus Capital Group AG ("Clarus Capital"). This document and the information contained herein are provided solely for information and marketing purposes. It is not to be regarded as investment research, sales prospectus, an offer or a solicitation of an offer to enter in any investment activity or contractual relation. Please note that Clarus Capital retains the right to change the range of services, the products and the prices at any time without notice and that all information and opinions contained herein are subject to change.

This document is not a complete statement of the markets and developments referred to herein. Past performance and forecasts are not a reliable indicator of future performance. Investment decisions should always be taken in a portfolio context and make allowance for your personal situation and consequent risk appetite and risk tolerance. This document and the products and services described herein are generic in nature and do not consider specific investment objectives, financial situation or particular needs of any specific recipient. Investors should note that security values may fluctuate, and that each security’s price or value may rise or fall. Accordingly, investors may receive back less than originally invested. Individual client accounts may vary. Investing in any security involves certain risks called non-diversifiable risk. These risks may include market risk, interest-rate risk, inflation risk, and event risk. These risks are in addition to any specific, or diversifiable, risks associated with particular investment styles or strategies.

Clarus Capital does not provide legal or tax advice and makes no representations as to the tax treatment of assets or the investment returns thereon, either in general or with reference to specific client's circumstances and needs. Recipients should obtain independent legal and tax advice on the implications of the products and services in the respective jurisdiction before investing. Certain services and products are subject to legal provisions and cannot be offered world-wide on an unrestricted basis. In particular, this document is not intended for distribution in jurisdictions where its distribution by Clarus Capital would be restricted. Clarus Capital specifically prohibits the redistribution of this document in whole or in part without the written permission of Clarus Capital and Clarus Capital accepts no liability whatsoever for the actions of third parties in this respect. Neither Clarus Capital nor any of its partners, employees or finders accepts any liability for any loss or damage arising out of the use of all or any part of this document. Source of all information is Clarus Capital unless otherwise stated. Clarus Capital makes no representation or warranty relating to any information herein which is derived from independent sources. Please consult your client advisor if you have any questions.